Best Practices From Kurt Salmon

The retailing landscape looks much as it did in the throes of the Great Recession. Unemployment remains persistently high, consumers lack confidence in the economy, and talk of a global economic crisis is everywhere.

But move in closer and the picture is more complex and detailed than it was three years ago. Despite the barrage of bad news and feeble macroeconomic growth, consumers have returned to old habits — spending at unprecedented levels, in fact.

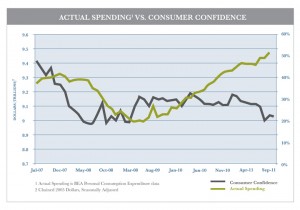

Consumer confidence, once closely linked to spending, hovers near 30-year lows. But as the chart below shows, actual spending has bounced back—hitting an all-time high of $9.5 trillion in September.

Furthermore, a modest 4% gain in income and a 34% drop in the savings rate over the past year slightly outpaced inflationary pressures (e.g., increased housing, health care and fuel prices). Combined with a 2% drop in consumer debt (see next chart), these factors mean employed consumers have more money to spend.

The American consumer appears to be on a precipice, precariously balanced between very modest personal gains and the increasing drag of high long-term unemployment and a staggering deficit. Many are calling this the “new normal,” a position of perpetual uncertainty and ongoing anxiety.

The New Normal: A Consumer Divided

In fact, the new normal is that the American consumer can no longer be summed up as a single shopper. The new normal is the trifurcation of our economy among the long-term unemployed and underemployed, the lower- and middle-class at risk of slipping into poverty, and high-income earners.

Unemployed and underemployed. Obviously, the post-recession era has been particularly difficult for the unemployed and underemployed, who are living week to week and barely making ends meet. With little or no access to reasonable credit, this cash-strapped population flocks to retailers sensitive to their need for frugality. And successful dollar stores appear to be just that, with some selling individually wrapped rolls of toilet paper, off-brand cereals at less than half the cost of grocers’ private-label brands, or even small apparel items, for about a buck.

At-risk middle-class. Formerly the hallmark U.S. shopper—the solidly middle-class consumer, who flexed so effortlessly from the aspirational luxury of Nordstrom to the fun, frugal fashions of Target—is fading. In that place are middle-class consumers who are employed and, for the most part, comfortable but weary from ongoing uncertainty and the very real possibility of slipping into underemployment.

While deeply anxious about the economy—only 21% say they’re confident in the economy, 1% fewer than the lowest-income Americans—these consumers are also still extremely brand conscious. In general, they are still committed to their favorite brands, but want a price point that gives them access to the experiences and products they have grown to love without compromising their need to be incredibly selective with their spending.

High-income earners. While only 28% of high-income earners say they feel confident in the economy, they’re back to pre-recession spending habits. While a bit skittish immediately following the Great Recession, these consumers have bounced back to new spending heights, powering noteworthy gains in traditional luxury categories. These consumers want the opulence of their beloved brands, without compromise, and they have the means to afford it.

Despite their differing economic situations, there is one commonality all three segments share: Brands still matter. Because overabundance and ubiquity continue to be the norm, all consumer groups have access to seemingly limitless assortments of nearly any item at almost any time.

Competing on price or a specific product attribute alone isn’t enough. Whether they have $5 or $500 to spend, all three consumer groups have the luxury of spending their hard-earned dollars at a variety of retailers. Beyond just amassing more stuff, these consumers want connection. Retailers and brands that can forge these connections—through a combination of product and experience—will be better positioned to win their target consumers’ hearts and dollars.

Winning Tactics

We see three winning tactics to help retailers navigate through ongoing economic uncertainty and an evolving marketplace.

Create a value orientation. No matter the target, retailers and brands must provide consumers with an accessible entry point to their products and experience. The key is to drive real and perceived value without compromising the brand.

Consider Apple. The retailer has been extremely successful at making its products available across the price spectrum without compromising its brand. Whether it’s a $49 iPod shuffle or a $249 iPod Classic, the consumer knows she is purchasing a high-quality product—and compelling experience—consistent with Apple’s reputation.

Shareholder pressure for short-term gains will continue to drive the temptation to pawn brand attributes for a short-term cash-out. But resist. Competing on deep discounts and promotions, devaluing product and experience to pinch pennies, gutting ancillary support to the purchasing cycle—now more than ever these tactics have the potential to destroy your brand in the not-so-long run.

Invest in experience. Differentiating your brand from competitors is more important than ever, and creating a compelling experience is one essential way to make your brand stand out.

A great customer experience offering is no longer optional, especially as other retailers step up their games. In fact, 83% of top retail executives recently surveyed by Kurt Salmon say improving the customer experience is a top investment priority for 2012.

Further, all consumer segments demand experience; targeting lower-income consumers doesn’t exclude a brand from this new mandate. For example, for lower-income targets, experience may be all about convenience. Kohl’s, for instance, successfully stole share from traditional department stores anchored to malls by opening more convenient, smaller-format stores closer to suburban residential hubs.

As margin pressure increases, many retailers will be tempted to skimp in this area. But as the economy regains strength, those who have invested in experience during this period will emerge with a competitive advantage.

Invest in preemptive distribution. Again, during periods of uncertainty, leaders will continue to invest in key areas. Given the accelerating trend toward preemptive distribution, top brands and retailers are moving beyond multichannel distribution—i.e., separate inventories for each channel—toward omnichannel distribution, one inventory and product flow across all channels.

Note these prime examples. eBay recently opened a window display on Park Avenue in New York. The display features selected products plus QR codes that consumers can scan with their phones to purchase a product or access more information. Procter & Gamble just set up virtual stores in several European subway stations, so busy commuters can scan QR codes to purchase items like razors and dish soap that will then be shipped to their homes. And in some Asian countries, consumers can now do all their grocery shopping while waiting for the train. Selecting items using QR codes on large plasma screens set up at stations, these time-strapped shoppers select all their grocery items and then check out and arrange for home deliveries.

As the retail environment changes, winning will take an evolving set of characteristics. Not so long ago, Walmart was winning on price alone; now Amazon is winning not only on price, but on assortment, convenience and preemptive distribution. In 2012 and beyond, retailers that are able to offer not only price and convenience, but also a compelling customer experience, will have the long-term competitive advantage.