Best Practices from Kurt Salmon

Many retailers are striving to better respond to changes in consumer demand, and it’s easy to see why: They’re pressed to reduce inventories and cut supply chain costs at the same time that the shopping patterns of American consumers have become virtually impossible to predict.

Making matters even more complicated, consumers now have unprecedented access to an infinite number of products and a virtually limitless number of places at which to buy them. They expect to be able to buy exactly what they want exactly when they want it, and if one retailer can’t make that happen, another one (or a dozen others) can.

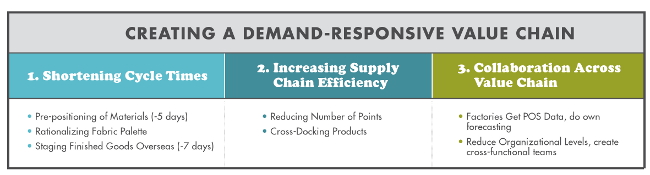

That’s where a demand-responsive value chain comes in. By shortening cycle times and increasing collaboration across the value chain, retailers can ensure they have the right product, in the right place, at the right time.

1. Shortening Cycle Times

Many retailers are beginning to move production closer to home (leveraging data to inform smarter decisions on the best manufacturing locations) as a way to shorten cycle times. Shorter cycle times can improve responsiveness to demand and increase inventory effectiveness.

The global product margin metric measures the cost from each point of manufacture to each point of distribution and the unique retail price from that point of distribution. Keeping this number in mind allows retailers and wholesalers to optimize total margin by choosing the best manufacturing locations based on discrete costs from multiple points of supply to multiple points of distribution and the retail price at each point.

But after a retailer’s sourcing decisions have been made, there are still several steps that can further decrease cycle times.

For example, consider a retailer that sources out of China and ships its products to the U.S. by boat. The industry standard cycle time for this situation is about 65 days from purchase order to store shelf, but leading retailers have been able to cut this down to about 50 days using several creative tactics.

One of the most effective ways has been to pre-position materials and capacity, which can save up to five days. Many market leaders have started pre-positioning materials, especially retailers who have large enough volumes to command the attention of mills. VF and JC Penney are prime examples.

To enable pre-positioning, it’s essential to take a fabric-first approach to the product development process. Start with a careful look at fabrics used across departments and rationalize the fabric palette. This is especially useful when it comes to basics. For example, different departments may be using 10 different weights of cotton that the consumer sees as identical. By rolling this demand together into fewer core fabrics, retailers can find synergies: less risk in each fabric order with higher quantities, better leverage to reserve capacity with mills and lower costs.

A mass discount retailer and a specialty apparel wholesaler both rationalized their fabric palettes, reducing the number of fabrics they used from more than 400 to fewer than 200, and saved tens of millions of dollars as a result. Another specialty apparel wholesaler created a program to help guarantee the availability of the key Italian wool it uses in one of its signature products, ensuring consistency and keeping costs down. But the challenge is not simply to reduce the number of fabrics on a single occasion, but instituting discipline within the organization to ensure fabric numbers don’t slowly creep back up.

However, pre-positioning does come with its challenges. First, the ability to accurately predict global demand is essential, but is often difficult for organizations with regional buying. Additionally, it’s imperative that mills, factories and retailers have a clear understanding of where materials will be stored and who will own the fabric liability from the outset. Some retailers prefer to procure, own and store all their fabric at the factory, while other retailers contract to use a certain amount of fabric while the factory maintains ownership of it. This becomes a negotiation and strategic question about a retailer’s level of trust with the manufacturer and desire to keep liabilities off the balance sheet.

However, pre-positioning does come with its challenges. First, the ability to accurately predict global demand is essential, but is often difficult for organizations with regional buying. Additionally, it’s imperative that mills, factories and retailers have a clear understanding of where materials will be stored and who will own the fabric liability from the outset. Some retailers prefer to procure, own and store all their fabric at the factory, while other retailers contract to use a certain amount of fabric while the factory maintains ownership of it. This becomes a negotiation and strategic question about a retailer’s level of trust with the manufacturer and desire to keep liabilities off the balance sheet.

In addition to pre-positioning materials, leading retailers are staging finished goods overseas, which can trim up to seven days from the average cycle. Leading apparel wholesalers and retailers store finished goods closer to production, where warehouse space is cheaper. Vendors or factories will commonly hold up to four weeks of supply, which helps reduce cycle times because orders can be filled directly from the stock instead of having to first be cut, sewn and packed.

2. Increasing Supply Chain Efficiency

Increasing supply chain efficiency can cut cycle times by an average of three days. More and more retailers are speeding up their domestic supply chain by cutting the number of stages a product has to move through or by reducing storage points.

A prime example of this is crossdocking, or moving just-received shipments to another location or directly to the store rather than receiving them into distribution center stock. More and more retailers are cross-docking products, eliminating time spent in storage (Walmart cross-docks about 85% of its volume). And as more retailers jump onto the cross-docking bandwagon, it will become more of an imperative for suppliers to support the capability as well.

3. Collaboration Across the Value Chain

Improving collaboration helps increase visibility into demand and creates a sense of shared accountability for decisions across the value chain. While increased collaboration is not a new topic, it is increasingly important as the value chain becomes ever more complex. Leading retailers have excelled at removing the barriers to collaboration and creating trusted relationships with vendors, but others are struggling and missing out on tremendous flexibility and savings as a result.

Improved collaboration means that factories develop core competencies that allow them to provide better service. Some factories are capable of taking POS data from retailers and creating forecasts for replenishment orders, which saves time and reduces supply chain work-in-process. For example, JC Penney sends POS retail data directly to the factories, which enables factories to forecast demand, buy fabric just in time, and cut it to a particular SKU or size immediately. The factory can then speed the process even further by shipping the finished garments directly to JC Penney stores.

Achieving improved collaboration does require overcoming a few hurdles. First, a lack of cross functional teams, processes and calendars makes collaboration difficult. Second, the right organizational design must be in place to facilitate, instead of hinder, the easy sharing of data between retailer and vendor. Tiered organizational structures that introduce unnecessary levels between the supplier and the point of demand add complexity and make it harder to share data.

But despite the potential difficulties associated with creating a demand responsive value chain, it’s something retailers cannot afford to ignore. The modern consumer already expects access to whatever she wants, wherever and whenever she wants it. And the trend is only intensifying as more exclusive and custom products add complications in forecasting and distribution. The implications to a retailer’s operations, from product development through supply chain and marketing, are significant. But even more significant is the cost of not developing a demand-responsive value chain.