There’s a growing disparity in the way some economic data have moved since the recession. On the one hand we have employment and income figures, which tell the story of a sluggish U.S. recovery with a long way to go to pre-recession prosperity. On the other hand, healthy retail sales and consumer spending have rebounded to, and even surpassed, pre-recession levels.

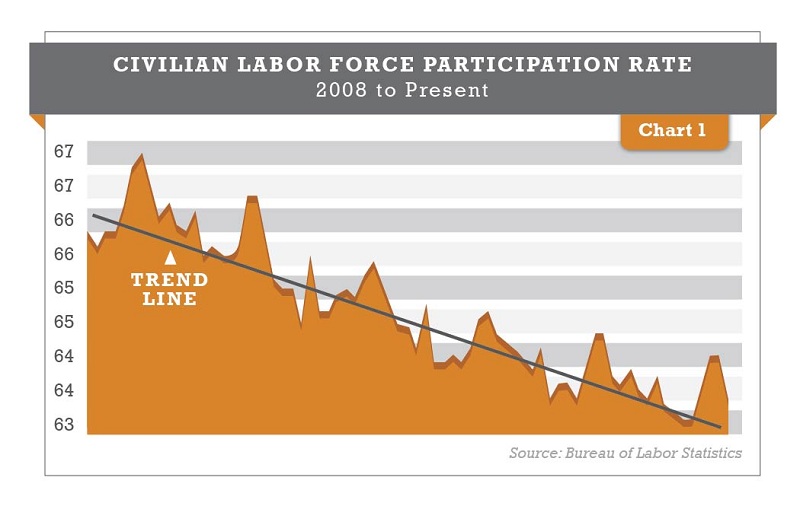

According to the Bureau of Labor Statistics, the population of working-age people has grown by more than 5 million since the beginning of 2008. The labor force has increased by only 1.5 million, and the total number of employed has decreased by 2 million, resulting in a steady decline in the labor force participation rate (see Chart 1).

That doesn’t jive with the brisk pace of consumer spending (Chart 2), according to Bernard Baumohl, Chief Economist at Princeton, NJ-based forecasting firm The Economic Outlook Group, who noticed the sudden divergence between total personal consumption expenditures and the labor force participation rates that began during the Great Recession.

That doesn’t jive with the brisk pace of consumer spending (Chart 2), according to Bernard Baumohl, Chief Economist at Princeton, NJ-based forecasting firm The Economic Outlook Group, who noticed the sudden divergence between total personal consumption expenditures and the labor force participation rates that began during the Great Recession.

The stubbornly high unemployment rate makes even less sense in light of retail sales which, according The Department of Commerce, have been growing by 3-5% per month over the last two years on a 12-month smoothed basis, as shown in Chart 3 below. Sales of durable goods have been particularly strong.

This is consistent with an unemployment rate much lower than the current rate of 7.3%, according to Baumohl, who noted: “… Not since the government first released retail sales on a monthly basis have we seen retail sales grow at such a vibrant pace with the unemployment rate so high.”

This is consistent with an unemployment rate much lower than the current rate of 7.3%, according to Baumohl, who noted: “… Not since the government first released retail sales on a monthly basis have we seen retail sales grow at such a vibrant pace with the unemployment rate so high.”

All this has been going on while, according to the Bureau of Labor Statistics, median household income has been on a steady decline (Chart 4).

How are all these unemployed consumers with declining incomes able to keep shopping?

How are all these unemployed consumers with declining incomes able to keep shopping?

As it turns out, being unemployed doesn’t necessarily mean not working. According to research by Professors Richard Cebula of Jacksonville University and Edgar Feige of the University of Wisconsin-Madison, a significant part of the U.S. population participates in the shadow economy, an estimated $2 trillion underground market in the U.S. These folks are doing everything from giving piano lessons to running retail stores. They’re being paid off the books in cash by their employers and/or customers, and either not reporting or underreporting their income.

We’re not just talking about mob bosses or drug dealers here, but about millions of people, some (but by no means all) of them undocumented immigrant workers, with everyday jobs, many in service businesses such as child care, landscaping, and construction. Much of the underreporting of income starts as a way to make ends meet after being laid off, but ends up becoming a lifestyle.

According to Professor Cebula, the underground economy has been around for as long as income tax. Its participants range from hardcore criminals to people whose lousy bookkeeping skills cause them to accidentally underreport their income. His research shows that in the last 10 years, the ratio of unreported and underreported adjusted gross income to reported AGI has ranged between 22% and 24%. Most of the underground income, says Cebula, is earned by people in the lowest income brackets.

To uncover this trend, Cebula and his colleagues simply followed the cash. Despite the proliferation of credit cards, debit cards, smart phone payment apps and bitcoin, currency in circulation with the public totals around $3,000 per capita, hardly the trappings of a cashless society. The Federal Reserve reports almost double-digit increases in currency outstanding over the last few years, to almost $1.2 trillion, compared to $800 billion six years ago (Chart 5).

The evidence is everywhere: people pulling out wads of cash in stores to pay for big-ticket items; small stores who “don’t charge you sales tax” if you pay them cash (which means they’re not reporting the revenue to the IRS); soaring demand for prepaid debit cards (which you can buy anonymously and use to pay utility, rent and other bills); the rise in underbanking and nonbanking. According to the FDIC, in 2011 the number of U.S. households with no bank accounts was 8.2%, up from 7.6% in 2009.

The evidence is everywhere: people pulling out wads of cash in stores to pay for big-ticket items; small stores who “don’t charge you sales tax” if you pay them cash (which means they’re not reporting the revenue to the IRS); soaring demand for prepaid debit cards (which you can buy anonymously and use to pay utility, rent and other bills); the rise in underbanking and nonbanking. According to the FDIC, in 2011 the number of U.S. households with no bank accounts was 8.2%, up from 7.6% in 2009.

Why is the economy’s dirty little secret not getting more air time? Well, for starters, it’s neither politically correct nor expedient to go after the little guy. It makes government look boorish, and after all, many of the people perpetuating this fraud are voters, so politicians have every incentive to turn a blind eye.

A more important factor, however, is that much of the $2 trillion ultimately goes into cash registers, and might have kept the real economy from tanking a few times during the recovery. Which means retailers aren’t exactly unhappy about it.

The U.S. is not the only country experiencing this trend. The shadow economy in Europe will total $3 trillion dollars this year, according to an A.T. Kearney/Visa report. In Italy, where the top personal income tax rate is 45% and tax evasion is practically a national pastime, it represents a massive 21% of GDP.

So is the shadow economy a good thing? Unless you’re a fan of felony tax evasion, of course not. The impact on government revenue is staggering, with an estimated $500 billion in lost federal income tax, money that could close the budget deficit (and possibly even create a surplus), reduce the national debt, help pay for improved infrastructure, and provide public services to people. Many of the people working off the books also collect unemployment or disability, go on Medicaid, and use food stamps, multiplying the fraud.

Of equal concern is the fact that the rapid growth of the underground economy since the recession might be a result of deeper and potentially more damaging trends: an underlying distrust in government; a feeling that regulations are too stringent and complicated; a lack of confidence in financial markets; declining confidence and hope. These feelings weren’t exactly soothed by the most recent government shutdown.

The Economic Outlook Group’s Baumohl feels that although impossible to quantify, the size of the underground economy could be as high as 10% of GDP. If legally accounted for, this $2 trillion would add another 10% to disposable income data in the U.S., and add a whopping 25% to government tax revenue.

Cebula feels that it would be impossible to collect tax on these transactions, however. First, because these transactions leave no paper trail and, in many cases, are done by people that the government doesn’t even know exist, it would be hard to find them. Second, even if uncovered, the taxation would be very short-lived. “In theory, if we were to tax it,” he added, “the behavior would stop, so there would be nothing to tax. And many illegal immigrants would just leave.”

In other words, trying to go after these people wouldn’t necessarily boost tax revenues very much, but would help curtail illegal activity and reduce the illegal immigration problem? Sounds like a step in the right direction.

However, Cebula’s argument fails to take into account the fact that plenty of the underreporting is done by businesses and households who, rather than get caught and pay penalties, might decided to improve their reporting record. That includes the dog groomer or handyman who doesn’t charge you tax if you “make the check out to cash.” He’s not going to turn away business; he’ll just do more of his business on the books. Maybe his prices will go up a bit in the short run, but they’ll eventually settle at what the market will bear, or he’ll find another line of work. So, theoretically, some of the tax gap will be at least partially recouped.

People who work off the books are hurting themselves in both the short and long terms. They’re not paying into Social Security or receiving health benefits. They can’t report abusive employers to authorities. They don’t participate in financial markets to build up investment income nest eggs. This is ultimately a drag on economic growth, which will hurt the retail industry.

The underground economy disfavors law-abiding people and shifts liabilities to future generations. Allowing businesses to get away with cheating makes it harder for legitimate ones to compete. The reduction in workforce participation puts upward pressure on labor costs, and places honest retailers, who collect and remit sales tax and abide by employment laws, at a price disadvantage.

The IRS claims to lack the resources to go after the tax cheats, which only makes the problem worse. When there are fewer police cars on the roads, more people speed. But how could it not be cost-effective to enforce compliance? When such a huge amount of owed taxes is not being paid, it shouldn’t take long for an IRS agent making $60,000 a year to earn the agency back his salary. We can’t afford to not force compliance. If successful, it might eventually lead to lower income tax rates for all which, as we know from history, tends to stimulate economic growth.

We need fewer regulations and red tape for businesses and households who employ people, and better enforcement of (simpler) tax laws. We need politicians to worry less about getting re-elected, and more about increasing government efficiency. And we need a level playing field that rewards success and honesty, punishes criminals, and helps people who really need help. Without these things, neither the free market nor democracy works.