The long-anticipated merger of two powerhouse European supermarket operators finally happened this summer. The merger of the two firms—Ahold of The Netherlands and Delhaize of Belgium—has great implications for food retailing in the U.S., far more than in Europe.

The long-anticipated merger of two powerhouse European supermarket operators finally happened this summer. The merger of the two firms—Ahold of The Netherlands and Delhaize of Belgium—has great implications for food retailing in the U.S., far more than in Europe.

That’s because the combined entity, known as Ahold Delhaize, operates a battalion of 2,000 supermarkets along the East Coast, from Maine to Georgia. That makes it one of the biggest players in the country. In total, Ahold Delhaize runs 6,500 food stores in 11 countries, but generates about two-thirds of its combined annual sales volume of $61 billion in the U.S.

Ahold will add its Stop & Shop and Giant supermarkets to the merger, along with its Peapod home-delivery business. Delhaize brings in Food Lion and Hannaford Bros. supermarkets. The FTC required the divestiture of 86 Ahold or Delhaize supermarkets, which went to several different buyers. Those sales won’t much change competitive dynamics along the East Coast, but forging a stronger Ahold Delhaize could create trouble for Publix, Wegman’s, Albertsons and others.

The combined company will be 61 percent owned by Ahold and have its world headquarters in The Netherlands. The CEO will be from Ahold.

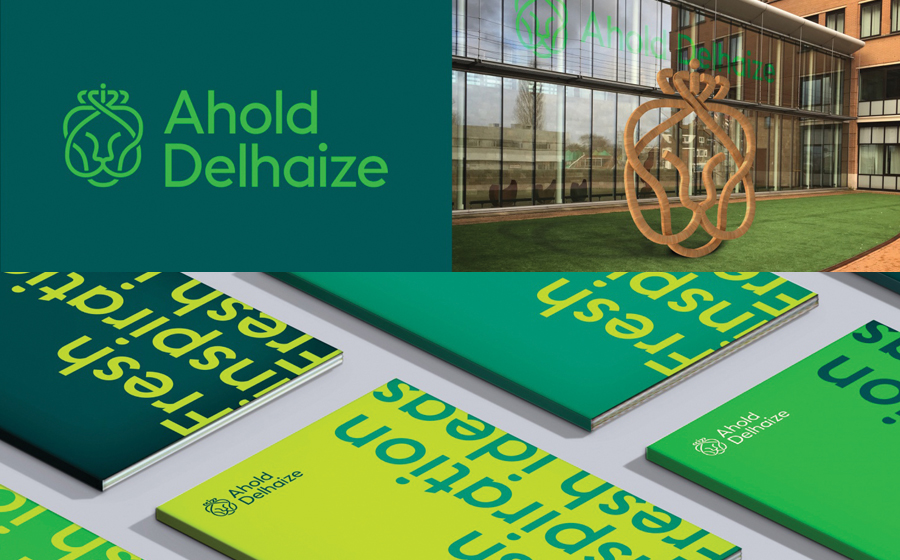

WHAT’S IN A LOGO?

The move has big implications. Before we get too deep into the weeds, let’s take a quick look at one minor but strange aspect of the deal: the new logo for the combined companies.

What is the new logo? A bizarre figure with an odd haircut? A pear? An upside-down heart? Idle scribbling? Or what?

To glean what it represents, it’s necessary to have some knowledge of the companies involved, as both have histories that stretch back more than a century. Ahold is also known as Royal Ahold. Delhaize is also known by a lengthy French name that includes “Le Lion.” Atop the new logo is a crown image intended to evoke royalty. The rest of the swirls evoke a lion.

Designing a logo is no small proposition. Companies invest heavily in the process, hoping that their customers, clients and investors will understand the significance. The logo was designed by FutureBrand, London. One of its designers said— perhaps a little defensively—that the new insignia was intended to be “respectful and celebrating of the rich history of these strong brands … [and is] intentionally joyful, more friendly and welcoming.”

All this is fine, but a logo that requires that much explanation is likely to be cryptic to most members of the public. The logo is the public face of the brand. I believe the new logo is too inside baseball: important to those in the know, obscure to others.

Still, Ahold Delhaize won’t rise or fall because of a new logo. But it might rise or fall because of the reasons for the merger and the execution of the strategy behind it.

WHY MERGE?

In the U.S. there has been a big push to form massive food-retailing companies. Recently, several big supermarket companies have combined including Albertson-Safeway, Kroger-Harris Teeter and Southeastern Grocers holdings. Such mergers are justified because it’s difficult to increase profitability in the food-retailing sector simply by increasing price points or building numerous stores. That food retailing is a thin-margin business makes the quest for increased profitability even more challenging than it is for other forms of retail.

One of the few profit-building strategies left for food retailers is to merge with another company with the hope that it will cut costs. The savings become the new profit center. Ahold Delhaize claims that their merger will yield in excess of $500 million in synergies.

It’s not impossible that $500 million can be obtained, but the future cuts both ways. A difficult or protracted integration of the companies could just as easily result in higher costs, especially in the near term. Obtaining synergies is a complex undertaking involving technology, buying, distribution, private label, a huge work force and more.

Ahold has a precedent for the merger, as it been in the acquisition business in the U.S. for a long time. That’s how it obtained so many supermarkets here. And it has a consistent marketing spin for each one of the expansions. In the many years I’ve followed Ahold, I’ve noticed that its acquisitions were always accompanied by glowing expectations of synergies. I also recall that in many instances the synergies simply didn’t materialize, or were long delayed. This was described by Ahold as “digestion” difficulties. You can’t fault it for being ambitious.

But digestion aside, at one point Ahold had such a difficult time in the U.S. that the entire company nearly collapsed. There were numerous reasons behind the near-death experience, but certainly a failure to find economies of scale was one.

Delhaize also obtained its two U.S. chains by acquisitions over a long period and with much caution. Nevertheless, it has had a difficult time with its Food Lion chain in the South. It still remains a fixer-upper. This means that the combined company has a lot more on its plate than just worrying about synergies.

We’ll see how it turns out.

THE BIG PICTURE

Let’s consider the implications of the Ahold-Delhaize situation on other forms of retailing.

Let’s return to the new “Lion King” logo, since this is something of more than academic interest—symbols matter. The situation brings to mind Golub Corp., operator of Price Chopper supermarkets in upstate New York and New England.

As I reported in “The Robin Report” a couple of years ago, Golub set an ambitious plan to convert the 40-year-old Price Chopper banner to “Market 32.” Why would they do that? Generations ago Golub operated stores under banners that included the “market’ name, and Golub was founded in 1932. Do consumers care about those factors? How would they even know? Maybe the name change was way inside baseball and largely for internal consumption.

The tactic didn’t work out well. Now Golub is said to be seeking additional capital or planning to sell the chain in an apparent effort to underwrite the costly name change and store renovations. Those renovations were needed, but they could have been done without the financial angst of the marketing costs of the name change. It should be noted that Golub has denied that a sale is in the offing. But that’s to be expected in the early stages of any recapitalization.

In both merger cases names mean something. Logos matter. And you can’t fool the public. Which leads us to these observations that apply to any retail enterprise:

- If an extensive image change is undertaken, be certain that the new image communicates something that captures consumers’ interest and curiosity. Research it. Be sure it’s worth it. If the change is meaningless to consumers, nice try, but you’ve struck out.

- Mergers should have a solid business reason behind them in addition to elusive synergies that might result. If margin improvements are impossible, maybe there’s something wrong with the fundamentals of the business. In the case of food retailing, the fundamental difficulty is over-storing. That issue presents a problem more vexing for food retailing that it does for other forms of retail.

Here’s why: if Macy’s closes a store it’s unlikely that another full-line department store will occupy the closed space, so over-building has been attacked. Conversely, a closed supermarket is likely to be occupied by another supermarket operator. Regrettably, the tough-love solution is for supermarkets to close in great numbers so that most won’t be absorbed by other food retailers.