The past several years have been rough on most retailers across all categories and levels. Some of the savviest merchants have responded to the challenging environment with a “stores-within-the-store” strategy, in which individual brands lease space and bring their own boutiques within the walls of a larger store, helping to turn that large space into a sort of mini-mall.

The past several years have been rough on most retailers across all categories and levels. Some of the savviest merchants have responded to the challenging environment with a “stores-within-the-store” strategy, in which individual brands lease space and bring their own boutiques within the walls of a larger store, helping to turn that large space into a sort of mini-mall.

There has been increasing excitement about this model, and it is starting to be deployed widely in range of stores. The model is usually a specialty brand leasing space within a department store. Though primarily seen in department stores like Macy’s and JC Penney, big-box retailers – both general, like Walmart and Target, and specialty, like Best Buy – have been using it as well.

The increasing popularity of stores-within-stores strategy isn’t hard to understand; the hope is that the outside brand will both drive traffic into the store and provide revenue through the rent they pay for the otherwise under-utilized floor space they occupy. Yet the model is not a panacea, and merchants need to approach it with a dose of caution and an even larger measure of analysis of purchase behaviors.

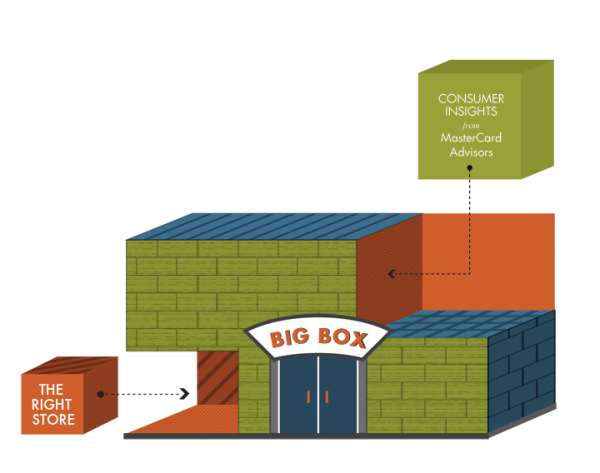

An effective stores-within-a-store strategy depends on synergy – both between the outside brand (or brands) and the host merchant, first of all, and also among the various boutiques collectively. The goal is for the various outlets to work together to create a compelling and unified shopping experience for the consumer, thus creating the kind of overall brand experience that results in more customers, and more purchases per customer.

Of course, there is something of an art to the process of picking the right retail partners, to arriving at both the global vision of the store as a whole and then identifying just those brands that will work best in that context. Something of an art, but as much a science, because truly successful decisions are based on hard data and the insights that careful analysis can yield.

There is a wide range of data available that can be of help to the merchant looking to host outside brands. First of all, it is necessary to begin with a baseline understanding of the store’s current performance – not just its year over year com-parisons, but its performance in relationship to its local competitors, or at least, a basket of them. We have seen retailers who were saved the expense of elaborate marketing campaigns when they discovered that what they thought were weak sales was actually a gain in market share in a weaker overall sales environment. It is only by having this kind of performance benchmark that a merchant can have a sense of what the store’s performance is and where it ought to be.

What kind of smaller stores or brands make for the best partners? Stores that are doing well, for one thing, and the same kind of performance benchmarking that merchants should use on their own establishments should be used to help identify the best of breed among prospective tenants. Additionally, the kind of stores that are doing best can come as a surprise; they may not be the best-known brands. At MasterCard Advisors, we have discovered that small merchants have been showing stronger year-over-year growth than the larger chains for each of the last nine months. By bringing in smaller businesses, large retailers can tap into their increased growth while adjusting a store’s mix to the tastes of the local market.

The way different kinds of stores interact can be a surprise as well. Conventional wisdom held that people generally keep their shopping to one tier, that a high-end consumer is a high-end consumer, and so on. But in examining aggregated transaction records, we discovered something very exciting: many consumers are perfectly happy to move back and forth among tiers, depending on the category. In fact, an average of 6.5% of a luxury shopper’s monthly spend is at bargain outlets. Likewise, value consumers are still crossing the street to make aspirational purchases on a regular basis.

What this points to is the need for the merchant to understand what his or her customers are doing once they leave the store. Where else are they shopping? What are they buying? If merchants can gain an understanding, through behavioral data, of which specialty stores their loyal customers are typically spending in when they’re not spending in their store, that knowledge can go a long way toward choosing the right brand partners. By using a large enough set of aggregated transaction data, it is possible to create a detailed behavioral model of a number of customer types, both current shoppers and desired customers. These models can be used to identify the kind of synergies that are already out there in the mind of the shopper, and need only the work of the creative retailer to bring them into the store and under its own roof.

The growth of e-commerce, the economic slowdown, the over-supply of retail square footage, all of these forces are acting to radically alter the retail environment, and the stores-within-stores strategy is one of the most exciting and creative responses we have seen. The rigorous use of robust data can turn a creative response into a winning one.