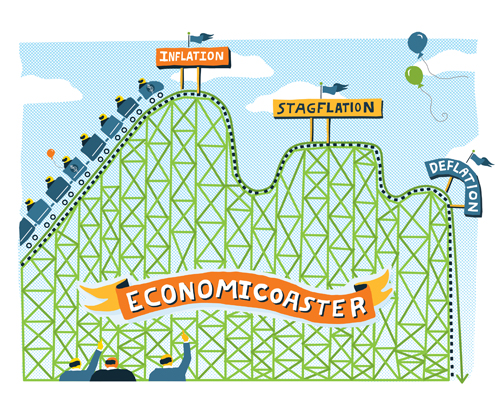

Now you see it. Now you don’t. This time I’m talking about the US economy falling into what may seem to be, and may feel like, inflation, but only for a nanosecond.

Now you see it. Now you don’t. This time I’m talking about the US economy falling into what may seem to be, and may feel like, inflation, but only for a nanosecond.

Then, like sleight of hand, we will seem to be entering into stagflation (high inflation coupled with high unemployment and stagnant demand).

But that too, will be for just a nanosecond.

Then, abracadabra, the final unveiling toward the end of 2011 and early 2012 will reveal what the economy has really slipped into. And, that would be deflation, or a decrease in the general price level of goods and services, occurring when the annual inflation rate falls below 0%, driven by high unemployment, stagnant demand and overcapacity.

This can turn into a spiraling cycle of price declines ultimately resulting in the feared “double dip” recession, if not worse.

Following is a scenario of how this journey unfolds.

The Illusion of Inflation

The Producer Price Index (PPI) has been increasing at accelerating rates for the past several months, rising 7.3% in May, excluding services and falling home prices. Intermediate goods prices rose an annualized 10.3% in the most recent month. Further, the broad retail sector, including most consumer goods wholesalers, have been railing for months about the rising cost of manufacturing, ingredient products, oil, food, international labor, transportation and distribution. All combined, cost increase estimates range anywhere from 10-20% across the board.

So, let the debates begin, about whether retailers should increase consumer prices, and/or about how much and in what categories to pare back on purchasing, in anticipation that consumers will buy less.

As of this writing and going into the last half of the year, retailers have made a combination of selective price increases and unit reductions based on lower forecasts for consumption.

In a true inflationary environment, characterized by too many dollars chasing too few goods and spawned by the Fed unleashing billions of newly minted dollars, buying back treasury bills and keeping the federal funds rate near zero, the theory goes that with all of this “free” money in the hands of consumers, they would not only accept higher prices, but buy two of something instead of one, anticipating that prices would increase even further. Accordingly, they would demand higher wages, driving businesses to raise prices again. Consumers and businesses would borrow more, ultimately driving government to increase interest rates, etc. and so forth. This is the upward inflationary spiral.

Well, the inflation theory doesn’t work in today’s reality. Of each dollar spent by the Fed, (of the total of $684 billion of new funds injected to-date into the banking system to jump-start lending and economic growth) less than 50 cents is making its way into the \”real\” economy. The current reality is that roughly 9% of the eligible workforce is still not employed, many having homes foreclosed upon (with home prices still dropping), and still trying to pay down debt while also increasing their savings rate. Businesses are sitting on close to $2 trillion in cash because they don’t see consumer demand justifying an investment in expansion and growth, (including hiring). So, this inflation won’t make it to anything that even looks like an upward spiral.

Instead, consumers are going to take money from their clothing, entertainment, “eating out” budgets, or other discretionary parts of their wallet, to pay for the rising prices of food, gas and other essential goods and services. And, the makers and sellers of all the non-essential stuff, who have selectively increased prices, will end up putting that stuff on sale and taking the hit to their bottom lines. And, they will buy fewer units going forward. Some retailers, like Dollar General, will not raise prices, publicly stating they would take the hit on gross margin growth to maintain or hopefully gain share of market.

So, what this situation might feel and look like is stagflation.

The Illusion of Stagflation

The Illusion of Stagflation

Stagflation, as named by British politician Iain McLeod in 1965, is characterized by high inflation coupled with high unemployment and stagnant demand. The US experienced a serious bout with it in the late 1970s, and many economists believe it was triggered by OPEC drastically increasing the price of oil.

The same triggers that lead to inflation – a flood of easy money, low interest rates and rising prices – can also drive stagflation. However, stagnant demand, accentuated by high unemployment, is also a required ingredient. So, in our current economic environment, it would seem that we are more likely to be entering a period of stagflation.

Professor Ronald McKinnon at Stanford University, who is also a senior fellow at the Stanford Institution for Economic Policy Research, takes us a step further in understanding the stagflation scenario. He believes global monetary fluctuations and the US failure to adopt an exchange rate objective, has caused the surge in inflation in emerging markets which ultimately loops around to a rising CPI in the US.

Secondly, he refers to the huge increase in excess reserves or “base money” in the US banking system, which has virtually tripled since 2008 as a result of the Fed’s spewing dollars into the system with the two stimulus packages, QE1 and QE2 (named from “quantitative easing,”) which were expected to be used for consumption and business investment and, ultimately, increased employment.

McKinnon specifically emphasizes the fact that the primary engine for increasing employment in economic recoveries has been the small and medium-sized business employers, or SME’s. And, their main source for working capital and credit lines is from the banks.

Well, as stated, along with the nearly $2 trillion of cash sitting in the coffers of large corporations not being invested in growth or hiring, the banks are also sitting on billions of “base money” reserves, and they are not lending. Neither has seen a return to consumption; indeed, they must be seeing stagnant demand.

So, stagflation it must be?

Not so fast. Don’t touch that dial. Do not be lulled into the belief that stagflation is the new normal, or reality. Reality will come in the form of deflation.

The Reality of Deflation

The Reality of Deflation

Deflation can be driven (or at least exacerbated) by high unemployment, stagnant demand and overcapacity. Its effect is economically catastrophic, and its vicious spiral of feeding on itself, ever-downward, makes it almost impossible to reverse, as demonstrated by Japan’s past two decades of struggling along the bottom.

My prediction, amidst the chatter and predictions of many economists about the dangers of inflation or stagflation, and as put forth in Issue 3 of The Robin Report late last year, is that many economists and business leaders will be confused by what I believe will be erratic cost and pricing dynamics going into the last half of 2011. And, the confusion will be heightened by the consumer response, which will ultimately lead to a clear understanding of the fact that we are not heading into inflation or stagflation, but caught in a deflationary cycle, similar to the one that housing is currently experiencing.

And, I have some not too shabby support for this prediction. Supply-side economics pioneer and Nobel Laureate Robert Mundell, as reported in the Wall Street Journal, said that dollar weakness (caused by QE1 and QE2, and leading to higher oil and commodity prices – a precursor to broader more damaging inflation), is not his main concern. Instead, he fears a return to recession later this year when QE2 ends and the dollar begins its inevitable rise. He states that deflation, not inflation, should be the greater concern.

The key point regarding his deflation prediction is that exchange rates transmit inflation or deflation into economies by raising or lowering prices for imported items and commodities. So, when the dollar declines significantly against the world’s second leading currency, the euro, commodity prices rise, which in turn creates US inflationary pressure. Conversely, when the dollar appreciates significantly against the euro, commodity prices fall, which leads to deflationary pressure.

So, just as the dollar declined against the euro from 2001-2007, due to the Fed’s suppression of the federal funds rate to pull us out of a recession, the same dynamics are occurring now, only with greater force (including QE1 and QE2), due to the severity of this recession.

Mundell tracks the monetary events to make his point. In response to the dollar’s decline during 2001-2007, investors diverted capital into inflation hedges, notably real estate, leading to the housing bubble and the horrific leveraging of global debt. He claims the bubble burst in 2007, followed by the Fed quickly reducing short-term interest rates, further lowering the dollar. However, as severe as the subprime crisis was, with looser money the economy seemed to be stabilizing in the second quarter of 2008. But then in the summer of 2008, Mundell says the Fed made one of the worst mistakes in its history: in the middle of the real estate crunch – made worse by “mark-to-market” accounting rules requiring banks to cover short-term losses, the Fed paused in lowering the federal funds rate. The result: in a few short weeks the dollar shot up 30% against the euro.

This dollar scarcity, according to Mundell, broke the economy’s back, led to the economic collapse and financial meltdown.

So, back to tried and true tactics goes the Fed. In March of 2009, they enact QE1, lowering the dollar against the euro, and we begin to feel a recovery. But, again, it’s another illusion, proven by the fact that in November of 2009, they ended QE1, and, again, the dollar soars over the euro pushing us back toward recession. So, what does the Fed do? They enact QE2, and again, it lowers the dollar and we are led to believe we are once again headed to recovery.

Then, I ask, if we are to believe Mundell’s prediction, what will happen when the Fed ends QE2 as they are expected to do in June?

Like a yo-yo, is not the dollar going to soar beyond the euro, just as it did twice before? And, if so, will we slip back into recession, including the dreaded deflation?

And, if we do fall backward again, will the Fed play a QE3 yo-yo? With the political pressure on our country’s debt and deficit, I don’t think so.

Mundell says that even if the Fed plays the loose money game again, it will just remain a band-aid, without curing the cancer. His solution: have the US Treasury fix the exchange rate between the dollar and the euro to maintain an upper and lower limit on the euro price, say between $1.30 and $1.40. He says over time the band would narrow to a given rate, and such a fixed exchange rate would allow prices to move free from the scourge of sudden deflation and inflation, allowing investment and planning timelines to expand along with production levels in Europe and the US.

But This Time It’s Different – And Worse

As much as I respect Robert Mundell and appreciate his brilliant view, and particularly because it adds great weight to my own prediction, I do believe there are a couple of additional and major points to be made about a difference between the recovery from the recession in the early 2000’s and the one we are currently “recovering” from. And, I believe they simply intensify Mundell’s prediction.

One big difference between then and now is that when the Fed loosened the money supply in 2003, the government, with the help of the “financial engineers” on Wall Street, found a new bubble to inflate to get the economy growing again: housing. And, as we now know, ‘growing’ was an understatement. As I have said before, it was more like a legal Ponzi scheme on steroids. Thus, the effects of its collapse were apocalyptic.

So, Ben Bernanke is left with a bigger mess than his mentor had faced. And, worse, do you see any new growth bubbles forming that Wall Street can work its alchemy to spread the risk and outsized profits around the world? I don’t think so.

There are some murmurings among economists that a new tech bubble is inflating once again, this time in its third iteration, with a focues on consumer markets, every pricing and promotional gimmick you might conjure up, social networking, etc. and so forth.

However big the potential of this bubble might be, I do not believe it has the leveraging power or the capacity for global finance to catapult entire economies around the world, as did the housing bubble.

The second major difference: overcapacity marches on; too many stores; too much stuff; and now a million web-site stores popping up on the Internet every day, all of which will drive deflation deeper and faster and longer.

Our “Managed” and Flawed Free Market System

As opposed to focusing on the demand side for consumption growth (where we have been since WWII), I suggest that we are, and have been for some time, facing a supply side problem that reveals a major flaw in our now somewhat ‘managed’ free market system.

Overcapacity is being perpetuated through new business entrants adding to the supply side at a faster rate than those leaving, and all of it compounded by slow and slower growth on the demand side. If this is so, it’s possible that no amount of stimulus to increase consumption will stop deflating prices, simply because a new paradigm now exists, with an eternal disequilibrium of too much supply driving an unrelenting downward pricing spiral.

As I’ve stated many times, everything is on sale all the time and shipped for free. Retailers have shifted their pricing structures (good, better, best), down. Outlet stores are growing faster than full price stores, even in the luxury sector. ‘Flash sales’ and ‘Groupon’ and all other kinds of on-sale online models are proliferating at the speed of light. What’s more, if you wait for two seconds, your smart phone will beep with an ad or a friend telling you where you can get whatever it is you’re thinking of buying, cheaper.

And, of course, the biggest undertow of them all is housing. As of this writing, home prices have dropped to the level they were in 2002, which essentially means that a decade of home equity just disappeared. As homes are consumers’ biggest investment in life, and a major source for spending dollars, the effect this continuing decline is having on the recovery is devastating. Worse, roughly 25% of homes were mortgaged at a higher value than the homes are now worth, and still falling. And, experts don’t see an end to this downward spiral. Sounds like a deflationary sector to me.

Across the entire marketplace, value is being recalibrated – down. And, it will continue, even as businesses “selectively” raise their prices to pass along inflating costs. They will not stick.

The Perpetuating Overcapacity

I maintain that even if demand were to increase, excesses on the supply side will continue to proliferate, because marginal players are not disappearing from the supply side quickly enough. The immutable theories from “Economics 101” are being reversed and we have no tracking or measuring devices to see such a fundamental transformation. The free market forces that have historically eliminated excess are impeded by:

The liberal and “strategic” use (or misuse) of bankruptcy during which businesses shed debt, renegotiate contracts and emerge as new low cost competitors. Overcapacity is preserved and the new company drives another round of price decreases.

- An endless pool of investment capital willing to “prop up” the losers or ostensibly to turn them around. In many cases they act as “vultures” whose ultimate goals are purely financial.

- An immeasurable and increasing global flow of new businesses adding to the supply side while consumption demand is either slowing or at least not balanced against supply, exacerbated by the two previous points.

- Finally, of course, the unrelenting acceleration of e-commerce, with virtually no barriers to entry, including financial. This is an unprecedented phenomenon, and there are no measures that indicate these enormous additions to the supply side are being offset by corresponding declines in the ‘brick and mortar ‘ or any other retail sector.

Can lower interest rates or extra dollars in the pocketbook stimulate consumer purchases in such an environment? I think not, at least not enough to absorb the relentlessly growing and excessive amounts of stuff being tossed into the marketplace, which has many markdowns built into it before it even hits the shelves, and tomorrow, and the next day, and the next, even lower.

And today’s consumer knows it, and doesn’t need it, and eventually will wait for tomorrow and the next day and the next. They are already behaving this way in the housing market, as it continues to plummet. Owning a home used to be considered an investment. Now it’s considered a risk.

So, the potential, and in my view, probability for deflation exists. However, it will be driven by infinitely growing overcapacity on the supply side.

What happens next? The hope is that the demand-side stimulants will elevate demand in tandem with some rationalization on the supply side, a shedding of the excess, so to speak. The result: a relative equilibrium of supply and demand, poised for a new round of healthy growth.

Don’t bet the bank on it.